Specialist Accounting for Optometrists & Optical Practices

Business Startup Specialism

20+

£0

50%

NHS

- Optometry Specialism: Optical practices have unique VAT complexities, NHS income streams and dispensing income analysis requirements that demand sector-specific accounting expertise. We find savings other accountants miss.

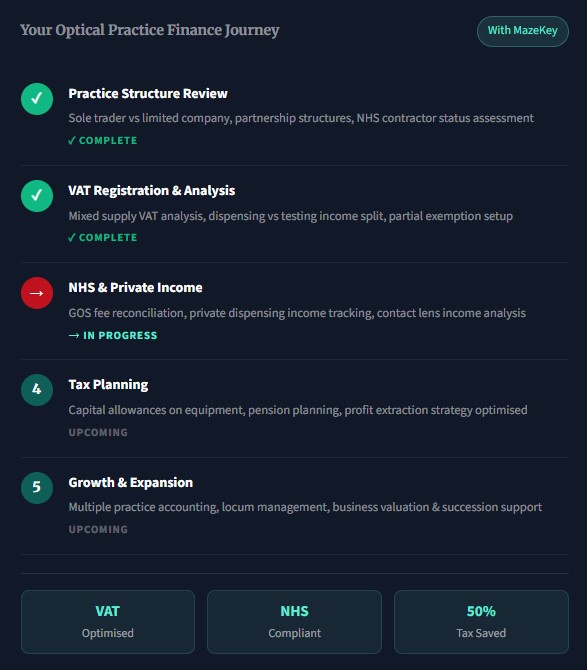

Optical Practice Finance Needs Genuine Sector Expertise

Optometry practices present accounting challenges that go far beyond standard small business accounting. The interplay of NHS and private income, the complex VAT position on mixed supplies, equipment capital allowances and the specific tax considerations for NHS contractors require genuine sector expertise.

Six Areas Where Optical Practices

Need Specialist Accounting

VAT handled correctly

Tax minimised legally

NHS income reconciled

Mixed Supply VAT Analysis

NHS GOS Fee Management

Tax Planning for Optometrists

Practice Structure Advice

Dispensing Income Analysis

Equipment Capital Allowances

A Full Specialist Service

Tailored to Optometrists

VAT Returns for Optical Practices

We handle the complex mixed supply VAT position of optical practices — analysing your income split between exempt services, zero-rated and standard-rated goods, calculating your liability correctly and filing every quarterly return accurately.

NHS GOS Income Reconciliation

Full reconciliation of your GOS fees, NHS payment statements and clawback positions — ensuring every pound of NHS income is correctly accounted for and any discrepancies are promptly identified and resolved with NHS England.

Annual Accounts & Tax Returns

Accurate annual accounts for your practice, corporation tax or self-assessment returns, and all Companies House or HMRC filing obligations managed professionally — with proactive tax planning built into every filing.

Profit Extraction Strategy

We advise on the most tax-efficient way to extract profits from your practice — balancing salary, drawings, dividends and pension contributions to minimise your overall tax burden and maximise what you actually take home.

Locum & Staff Payroll

Full payroll management for employed optometrists, dispensing opticians and practice support staff — plus guidance on the correct tax and NI treatment of locum optometrists, eliminating employment status risk.

Practice Growth & Valuation

Whether you’re opening a second practice, bringing in a partner or planning a future exit, we provide the financial modelling, due diligence support and practice valuation your decisions require.

How We Support Your Optical Practice

Free Practice Consultation

VAT & Income Review

Accounts & Returns Prepared

Filed & Submitted

Why Optometry Practices Face Unique Accounting Challenges

Optical Practice Finance

Needs Specialist Handling

Without Specialist Advice

vs With MazeKey

The Risk of Generic Advice

- Mixed supply VAT calculated incorrectly — HMRC penalties and backdated liability

- NHS GOS income not reconciled — clawbacks undetected, income unclaimed

- Equipment capital allowances missed — overpaying tax on every investment

- Wrong business structure — unnecessary tax burden on every profit pound

- No income analysis — management decisions made without financial visibility

Built for Practice Profitability

- Mixed supply VAT calculated correctly — HMRC compliant, liability minimised

- NHS GOS income fully reconciled — every payment tracked, every clawback challenged

- All capital allowances claimed — maximum tax relief on every equipment purchase

- Optimal practice structure — tax-efficient from the very start

- Locum payments correctly handled — employment status risk eliminated

- Detailed income analysis — management decisions informed by real data

Why Choose MazeKey for for Optometrists?

01

How does VAT work for an optical practice?

Optical practices make mixed supplies — eye examination services are VAT-exempt, while most prescription spectacle frames and lenses are zero-rated, and some items (non-prescription sunglasses, contact lens solutions) are standard-rated at 20%. This creates a complex VAT position requiring careful income split analysis, which we handle correctly on every quarterly return.

02

Do I need to reconcile my NHS GOS payments?

Yes, and regularly. GOS payments from NHS England should be reconciled against your patient records to identify any discrepancies, under-payments or clawback positions. We manage this NHS income reconciliation as a core part of our optometry accounting service — ensuring every pound of NHS income is correctly accounted for.

03

Should my practice be a limited company or partnership?

This depends on your profit level, NHS contractor status, number of principals and long-term exit plans. Generally, a limited company becomes more tax-efficient once practice profits exceed a certain threshold. We assess your specific situation and provide a clear, quantified comparison for your circumstances before making any recommendation.

04

How do I handle locum optometrist payments?

Locum payments require careful treatment for tax and National Insurance purposes. Depending on the arrangement, locums may be genuinely self-employed or caught by employment rules. We advise on the correct treatment for your specific arrangements and ensure your practice avoids any HMRC employment status disputes.

05

Can I claim capital allowances on my optical equipment?

Yes. All qualifying optical diagnostic equipment, dispensing tools, practice technology, fixtures and fittings can be claimed through capital allowances — potentially providing 100% first-year relief through the Annual Investment Allowance. We ensure every qualifying cost is correctly identified and claimed in full.

06

How much does optometry practice accounting cost?

We provide fixed-fee, transparent pricing tailored to the size and complexity of your practice — covering VAT, annual accounts, tax returns, payroll and NHS income reconciliation. The initial consultation is always free — we review your current position and identify any immediate savings before proposing a package.